fascinating that people didn't used to finance cars

02-19-18, 06:21 AM

02-19-18, 06:21 AM

#31

Lexus Test Driver

I think whatever car you plan on buying/leasing, it shouldn't be more than 10-20% of your income / cash on hand.

Now if your your young with no kids and obsesed with cars maybe you can go to 50%.

Having the cash to buy a car and actually using that cash to throw at a depreciating asset are very different.

It all depends on how much $$$ you have and your investment strategy. Personally there is no reason to pay cash if i can get a rate of 2% or lower, even if you put the money in a 5yr CD you will get a better return.

Now if your your young with no kids and obsesed with cars maybe you can go to 50%.

Having the cash to buy a car and actually using that cash to throw at a depreciating asset are very different.

It all depends on how much $$$ you have and your investment strategy. Personally there is no reason to pay cash if i can get a rate of 2% or lower, even if you put the money in a 5yr CD you will get a better return.

02-19-18, 06:36 AM

02-19-18, 06:36 AM

#32

Lexus Champion

I'm successful and financially secure myself. Never been in debt (except for a brief period when my house was new)....and never plan to. And, yes, fixed-income investments helped me take an early retirement. But that was also when interest rates were considerably higher than they are today. Today, you are lucky to get 3-4% on municipal bonds, though that is federally tax-free, and sometimes also state-tax-free.

Yes, you can make money with stocks if the market is timed right, but it is risky at best...and you pay capital gains tax to the IRS and state.

The best way to finance a car, of course, if possible, is to get a 0% loan...we sometimes see that with automakers with strong incentives to sell certain vehicles. Then, with essentially free money (even more so, counting for inflation), yes, any interest you earn on an investment will profit will help you pay off the loan.

Yes, you can make money with stocks if the market is timed right, but it is risky at best...and you pay capital gains tax to the IRS and state.

The best way to finance a car, of course, if possible, is to get a 0% loan...we sometimes see that with automakers with strong incentives to sell certain vehicles. Then, with essentially free money (even more so, counting for inflation), yes, any interest you earn on an investment will profit will help you pay off the loan.

02-19-18, 06:36 AM

02-19-18, 06:36 AM

#33

Lexus Fanatic

Yes...good point.  They can vary quite a bit from place to place, both from property values themselves, and from whatever property-tax rates local governments set. But, in most cases, they are less than what typical mortgages are. Unfortunately, under the new American tax law, only $10,000 worth is now deductible on the Federal Schedule A.

They can vary quite a bit from place to place, both from property values themselves, and from whatever property-tax rates local governments set. But, in most cases, they are less than what typical mortgages are. Unfortunately, under the new American tax law, only $10,000 worth is now deductible on the Federal Schedule A.

Since the thread topic is financing a car, I'd also point out that, at one time, interest on personal car-loans from a bank or other lending-institution was deductible on your Federal taxes. That changed with the tax laws of 1986, which eliminated that deduction, so, since then, a fairly common practice has been to use a home-equity loan (in other words....mortgage) to finance a car by putting up at least a portion of one's home as collateral. That's a risky move, IMO, but, of course, is done so that the interest (which is still fully-deductible, even on the new tax law) still gives one a tax break.

They can vary quite a bit from place to place, both from property values themselves, and from whatever property-tax rates local governments set. But, in most cases, they are less than what typical mortgages are. Unfortunately, under the new American tax law, only $10,000 worth is now deductible on the Federal Schedule A.Since the thread topic is financing a car, I'd also point out that, at one time, interest on personal car-loans from a bank or other lending-institution was deductible on your Federal taxes. That changed with the tax laws of 1986, which eliminated that deduction, so, since then, a fairly common practice has been to use a home-equity loan (in other words....mortgage) to finance a car by putting up at least a portion of one's home as collateral. That's a risky move, IMO, but, of course, is done so that the interest (which is still fully-deductible, even on the new tax law) still gives one a tax break.

Last edited by mmarshall; 02-19-18 at 07:10 AM.

02-19-18, 07:06 AM

#34

Lexus Fanatic

If the former then I would say that�s low, if the latter I would say that�s high.

02-19-18, 07:13 AM

#35

Lexus Test Driver

If your buying a $50k car in cash, that should not exceed 20% of your overall liquidity / marketable securities.

Financing / Leasing monthly payment should be 10% or less of your Net monthly income.

02-19-18, 07:32 AM

#36

Lexus Fanatic

02-19-18, 10:13 AM

#37

Interesting thread.

Discussions of this sort can often get folks bent out of shape, because we like to think we have a handle on how life works. It's kind of like sexual prowess--most guys think they are quite a bit better in bed than the average Joe, but mathematics says that just can't be.

There are folks that make their money in rapid-fire buy/sell daytrading. I have no idea how they are able to do it, but I suspect I'd be horrible at it. My mindset is to look at the long term: I think that, when measured over many decades, the stock market does about 8%. Okay, so I will put my money into the market and sit on my hands for decades. Buy individual companies? If I know the industry well and think my crystal ball is a bit more focused than most, then yeah. But it's far from a sure thing and folks get burned all the time.

Right now the market is climbing, as is real estate. Making profits now can be done by any sentient warm body. How about ten years ago? Did you sell off every asset you had before they declined 40%? I didn't.

Forgive me if I've already mentioned this brief story on this board. I like to tell it to my daughter's boyfriends though I doubt the moral sinks in: In 1982 I was a young sales rep for HP, selling minicomputers to the military in SoCal. One day during lunch I walked into a nearby Wells Fargo bank and, since I had a little extra cash, looked into these new-fangled "IRA" accounts (money goes in tax-free, grows tax-free, take it out and pay tax then). Went back to the office and my peers gently ridiculed me for picking the "Golden Guarantee" IRA. Why, there were some IRAs that paid 12-14% for three years, how could I turn that down? No, what I got was a guaranteed 10% per year--UNTIL I TURNED 60. I was betting that the sky-high interest rates back then were an anomaly and would eventually head down, which they did. A few years back I cashed out at $107,000. On a $6K investment. The miracle of compound interest. Was I a brilliant investor?--don't think so.

If anyone asks (and they don't), I'd say (1) make sure your outgo is less than your income, (2) put something aside out of every paycheck, (3) examine historical trends, but (4) expect the unexpected and don't freak when they come along. Oh, and the fact you are reading this on a Lexus message board means you are already unbelievably fortunate in the game of life. Enjoy your day, and cherish your friends and family.

Discussions of this sort can often get folks bent out of shape, because we like to think we have a handle on how life works. It's kind of like sexual prowess--most guys think they are quite a bit better in bed than the average Joe, but mathematics says that just can't be.

There are folks that make their money in rapid-fire buy/sell daytrading. I have no idea how they are able to do it, but I suspect I'd be horrible at it. My mindset is to look at the long term: I think that, when measured over many decades, the stock market does about 8%. Okay, so I will put my money into the market and sit on my hands for decades. Buy individual companies? If I know the industry well and think my crystal ball is a bit more focused than most, then yeah. But it's far from a sure thing and folks get burned all the time.

Right now the market is climbing, as is real estate. Making profits now can be done by any sentient warm body. How about ten years ago? Did you sell off every asset you had before they declined 40%? I didn't.

Forgive me if I've already mentioned this brief story on this board. I like to tell it to my daughter's boyfriends though I doubt the moral sinks in: In 1982 I was a young sales rep for HP, selling minicomputers to the military in SoCal. One day during lunch I walked into a nearby Wells Fargo bank and, since I had a little extra cash, looked into these new-fangled "IRA" accounts (money goes in tax-free, grows tax-free, take it out and pay tax then). Went back to the office and my peers gently ridiculed me for picking the "Golden Guarantee" IRA. Why, there were some IRAs that paid 12-14% for three years, how could I turn that down? No, what I got was a guaranteed 10% per year--UNTIL I TURNED 60. I was betting that the sky-high interest rates back then were an anomaly and would eventually head down, which they did. A few years back I cashed out at $107,000. On a $6K investment. The miracle of compound interest. Was I a brilliant investor?--don't think so.

If anyone asks (and they don't), I'd say (1) make sure your outgo is less than your income, (2) put something aside out of every paycheck, (3) examine historical trends, but (4) expect the unexpected and don't freak when they come along. Oh, and the fact you are reading this on a Lexus message board means you are already unbelievably fortunate in the game of life. Enjoy your day, and cherish your friends and family.

02-19-18, 10:22 AM

#38

Lexus Test Driver

What's wiser than being out of debt?  You won't be out of debt as long as someone else (or a bank) still has a lien on the car. Once the title is clear and it is legally yours, no one can take it away from you or repo it if you lose your job or otherwise can't pay the note each month.

You won't be out of debt as long as someone else (or a bank) still has a lien on the car. Once the title is clear and it is legally yours, no one can take it away from you or repo it if you lose your job or otherwise can't pay the note each month.

You won't be out of debt as long as someone else (or a bank) still has a lien on the car. Once the title is clear and it is legally yours, no one can take it away from you or repo it if you lose your job or otherwise can't pay the note each month.

02-19-18, 10:39 AM

#39

Lexus Fanatic

If anyone asks (and they don't), I'd say (1) make sure your outgo is less than your income, (2) put something aside out of every paycheck, (3) examine historical trends, but (4) expect the unexpected and don't freak when they come along. Oh, and the fact you are reading this on a Lexus message board means you are already unbelievably fortunate in the game of life. Enjoy your day, and cherish your friends and family.

02-19-18, 10:52 AM

#40

Super Moderator

Interesting thread.If anyone asks (and they don't), I'd say (1) make sure your outgo is less than your income, (2) put something aside out of every paycheck, (3) examine historical trends, but (4) expect the unexpected and don't freak when they come along. Oh, and the fact you are reading this on a Lexus message board means you are already unbelievably fortunate in the game of life. Enjoy your day, and cherish your friends and family.

Originally Posted by Wilkins Micawber

Annual income twenty pounds, annual expenditure nineteen pounds nineteen and six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds nought and six, result misery.

I have more than enough money set aside* to pay cash for our next car, but will likely finance anyway if the terms are good (sub-3%). There's a good chance that later this year I'll enough there to pay off my mortgage (2.5%), but no way in hell am I doing that. Cheap leverage FTW.

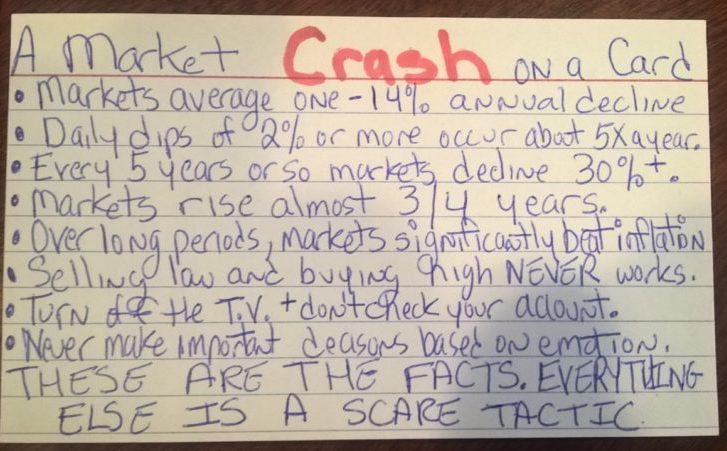

*in an investment account, of course, which returned 22% last year, and 1.5% so far this year despite the LARGEST SINGLE DAY MARKET DROP OF ALL TIME!!!!! (TM) (see last line of notecard above) earlier this month

Last edited by geko29; 02-19-18 at 11:01 AM.

02-19-18, 12:06 PM

#41

One clarification on your comment above, while it was the largest single day point drop in the Dow, at under 5% of the index it did not even make the top 20 in percentage drops. The largest drop percentage wise was "Black Monday", October 19, 1987 when the market dropped 508 pts, but it was 23% of the index.

02-19-18, 12:12 PM

#42

Lexus Fanatic

I agree with your overall comments. An analogy I heard several years ago about the stock market, is like riding a train. Get on the train and ride...don't get off and on at each stop. Never try to time the market.

One clarification on your comment above, while it was the largest single day point drop in the Dow, at under 5% of the index it did not even make the top 20 in percentage drops. The largest drop percentage wise was "Black Monday", October 19, 1987 when the market dropped 508 pts, but it was 23% of the index.

One clarification on your comment above, while it was the largest single day point drop in the Dow, at under 5% of the index it did not even make the top 20 in percentage drops. The largest drop percentage wise was "Black Monday", October 19, 1987 when the market dropped 508 pts, but it was 23% of the index.

http://www.businessinsider.com/sp-50...reakers-2015-8

02-20-18, 03:31 AM

#43

Super Moderator

Originally Posted by John C. Bogle

The idea that a bell rings to signal when investors should get into or out of the stock market is simply not credible. After nearly 50 years in this business, I do not know of anybody who has done it successfully and consistently. I don't even know anybody who knows anybody who has done it successfully and consistently.

One clarification on your comment above, while it was the largest single day point drop in the Dow, at under 5% of the index it did not even make the top 20 in percentage drops. The largest drop percentage wise was "Black Monday", October 19, 1987 when the market dropped 508 pts, but it was 23% of the index.

02-20-18, 07:34 AM

#44

That's not a clarification, it was my entire point about the financial **** industry and the reason I put it in all caps and added the "(TM) (See last line of notecard above)", which says "everything else is a scare tactic". They latch on to "OMG over a thousand point drop!" and fearmonger like crazy. Meanwhile, as you point out, that 1,175 points for early February's DJIA was just 4.6%, to the lowest value it had been since.....December 11, 2017. <yawn>. So let me get this straight, I'm supposed to be terrified of "the worst day ever", that didn't even erase two month's worth of gains, or trigger even the first of the three circuit breakers that Mike mentioned above? But I'm sure plenty of people did panic, thanks to the FP industry.

Folks need to first assess their risk tolerance and reaction to volatility, then invest accordingly.